The Weil European Distress Index – June 2022

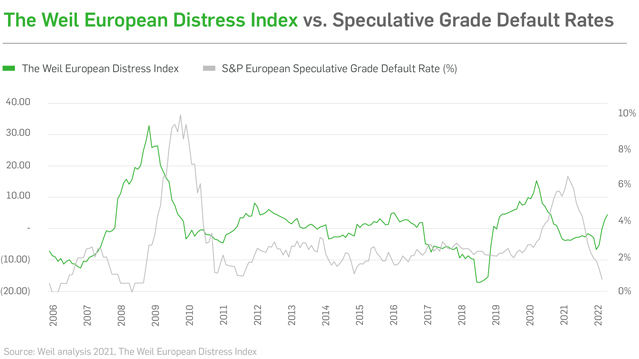

Corporate distress across key European markets rose to its highest level since August 2020, driven by pressures on risk, liquidity and financial markets, according to the latest Weil European Distress Index. The study, which aggregates data from more than 3,750 listed European corporates and financial market indicators, shows that large caps are experiencing the highest distress across all groups of European listed companies.

Increasing pressure around risk metrics, as well as a squeeze on liquidity, weaker investment and a sharp deterioration of market fundamentals, have all contributed to the rise over the past three months.

The findings come as countries across Europe face a cost-of-living crisis driven by supply chain issues arising from the aftershocks of the pandemic and the War in Ukraine. Central banks are starting to tighten monetary policy in response to 40-year highs in inflation, putting further pressure on spending, investment and highly leveraged companies. This is filtering through into an economic slowdown, with data pointing to a likely increase in corporate defaults.

Corporate distress can be defined as uncertainty about the fundamental value of financial assets, volatility and increases in perceived risk. It also refers to the disruption of the normal functioning of companies’ financial performance. There are several common characteristics of corporate distress: liquidity pressures, reduced profitability, rising insolvency risk, falling valuations and reduced return on investment.

Sector trends

The most distressed sector was Retail & Consumer Goods, driven by poorer investment and valuation metrics and a squeeze on liquidity. Having picked up sharply from well below-average levels at the end of last year, retailers and brands continue to face rising costs, supply chain disruption and labour shortages, along with 40-year highs in inflation which are eroding margins.

Distress across Travel, Leisure & Hospitality companies has eased since the reopening of economies and the ramping up of international travel. However, it remains the second-most distressed sector in Europe as profitability remains under intense pressure against the backdrop of rising costs and staff shortages.

Meanwhile, levels of distress across Healthcare businesses have risen sharply as the positive impact from the pandemic continues to wane. While remaining below the long-run average, distress has been pushed higher by pressure on liquidity and weaker investment factors.

Geographical trends

UK corporates reached the highest levels of distress since September 2020, driven by pressures around liquidity, investment and profitability. The Bank of England raised interest rates to 1.25% in June, the fifth consecutive hike as they carefully balance tightening monetary policy with economic growth. The UK is the second-most distressed country in Europe.

Distress across German corporates was the highest compared with other European markets. Levels of distress have not been higher since July 2020, in the midst of the global pandemic.

Despite a sharp rise in May, levels of distress across corporates in France remain below the long-run average. France is the only European country across Weil’s coverage where this is the case.

Corporate distress across Spain and Italy rose markedly in the latest period to its highest level since December 2020. This has been driven higher by weakening valuation metrics and pressure on liquidity, along with increasingly challenging market sentiment. Inflation in Italy (+6.9%) and Spain (+8.5%) have risen to uncomfortable levels, while the labour market in both countries is significantly weaker than other European nations.

Contributor(s)

More from the Restructuring Blog

Copyright © 2026 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Prior results do not guarantee a similar outcome. Weil, Gotshal & Manges LLP is headquartered in New York and has office locations in Austin, Boston, Brussels, Dallas, Frankfurt, Hong Kong, Houston, London, Los Angeles, Miami, Munich, New York, Paris, San Francisco, Silicon Valley and Washington, D.C.