Chesapeake Bond Redemption Case: Ambiguity, Plain Meaning and Value

Contributed by Brian Wells

Many readers likely are familiar with the basic tenants of contractual interpretation. The key is to give effect to the intent of the parties. Where contractual language has a plain meaning, that is the best indication of intent. Where language is ambiguous, a court can examine extrinsic evidence (i.e., evidence outside the four corners of the agreement, such as evidence of negotiations) to determine the parties’ intent. These are some of the more basic elements from the framework used by attorneys and judges in the pursuit of meaning. The recent Chesapeake Energy Corporation decision from the United States Circuit Court for the Second Circuit illustrates that, though the basic interpretive framework appears straightforward, in application it can be complex, difficult, and contentious. Depending on one’s perspective, this decision might serve as a cautionary tale – or a signpost for opportunity.

A Latent Dispute: Two Readings, One Text

The dispute at issue revolved around $1.3 billion of 6.777% senior notes Chesapeake issued in 2012 and, more specifically, an unusual redemption provision in the bonds’ indenture. The indenture generally provided that the issuer (Chesapeake) could not redeem the bonds unless it paid the holders a make-whole premium. During a specified window near the beginning of the notes’ term, however, the issuer had the option to redeem the notes at a significantly cheaper price of par plus accrued interest (i.e., without a make-whole premium). As will be described in more detail below, the issuer and the indenture trustee came to disagree on the precise contours of the window for early redemption at par.

Two sentences in section 1.7(b) of the supplemental bond indenture (the full text of this section and a related section is available here) established the window. The pertinent language from the section provided follows:

At any time from and including November 15, 2012 to and including March 15, 2013 (the “Special Early Redemption Period”), the Company, at its option, may redeem the Notes in whole or from time to time in part for a price equal to 100% of the principal amount of the Notes to be redeemed, plus accrued and unpaid interest on the Notes to be redeemed to the date of redemption . . . .

The Company shall be permitted to exercise its option to redeem the Notes pursuant to this Section 1.7 so long as it gives the notice of redemption pursuant to Section 3.04 of the Base Indenture during the Special Early Redemption Period.

Section 3.04 required notice of redemption to be mailed 30-60 days before the redemption date. The issuer contended that, so long as it provided notice of redemption within the Special Early Redemption Period, the actual redemption could occur outside the window within 30 to 60 days after the notice. The issuer read the word “redeem” in the first sentence to mean “commence the process of redemption,” i.e., to provide notice of redemption. Under this reading, March 15 would be the last day to provide notice of redemption, and May 15 would be the last possible day to redeem the bonds at par. For readers who are visual learners, here is the concept:

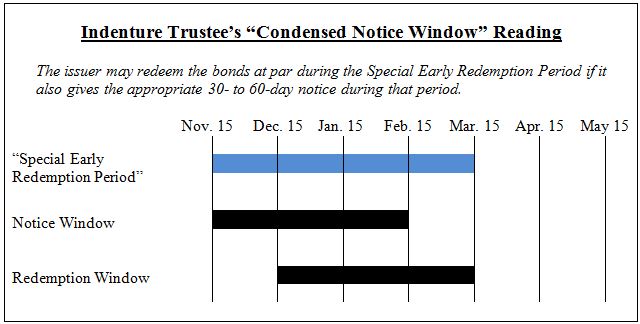

On the other hand, under the trustee’s reading, the issuer could only redeem the bonds at par by providing notice and completing redemption during the Special Early Redemption Period. Given the requirement that notice precede redemption by 30 to 60 days, the trustee argued that the indenture created two staggered time periods – a 3-month window to give notice (from November 15 through February 15) and a 3-month window to redeem the bonds at par (from December 15 through March 15). Again, here is the concept in chart form:

The Catalyst

On February 20, 2013, less than 30 days before the end of the Special Early Redemption Period, the issuer notified the indenture trustee of its intent to provide notice of a special early redemption on March 15. The trustee and a bondholder, though, argued that the last day to give the minimum 30-day notice for redemption within the Special Early Redemption Period was February 15, or five days before the issuer’s communication. The trustee thus refused to participate in a redemption at par on the basis that the time for a timely notice had passed. In addition, noting that the indenture provided that any notice to redeem would be irrevocable, the trustee informed the issuer that if it issued an untimely notice it would be deemed an irrevocable notice to redeem at the make-whole price.

The issuer was thus left to choose between (1) risking payment of a $400 million make-whole premium by potentially issuing an untimely notice and (2) foregoing early redemption altogether and losing the benefit from refinancing in a favorable interest rate environment. Caught between a rock and a hard place, the issuer mailed a conditional notice of redemption and filed a declaratory judgment action with the United States District Court for the Southern District of New York seeking confirmation (1) that the deadline to notice a special early redemption was March 15, and, alternatively, (2) that if the conditional notice was not timely to redeem the bonds at par, then the notice would be null and void and would not bind the issuer to redeem the bonds.

Judicious Interpretation

The filing and notice were followed by several weeks of expedited discovery and trial over the meaning of the language in the indenture. The district court issued a 93-page opinion concluding that the unambiguous language of the bond indenture supported the issuer’s expansive-window interpretation and that its conditional notice was timely to redeem the bonds at par. In an alternative holding, the district court found that even if the indenture was ambiguous, extrinsic evidence of negotiations between the issuer and the bond underwriter (which, notably, had never been revealed to the indenture trustee or the holders that purchased the bonds) proved that the drafters’ intent was to create an expansive early redemption window.

With the district court’s blessing, the issuer proceeded to redeem the bonds. Meanwhile, the trustee appealed from the district court’s decision to the Second Circuit. Months later, in a dramatic reversal, a panel for the Second Circuit concluded in a 2-1 decision that the bond indenture unambiguously supported the condensed-window interpretation, meaning that the issuer had not been entitled to redeem its already-redeemed bonds at par because it had failed to provide timely notice. The majority remanded the case to the district court to determine whether the redemption notice for the already-redeemed bonds should be deemed a notice to redeem at the make-whole price (an issue worth at least $400 million).

The dissenting judge also issued an opinion, which noted the conflicting interpretations of the district and circuit court judges and (on this and more technical interpretive grounds) concluded that the language was ambiguous, meaning that extrinsic evidence should have been consulted to determine intent. Though the dissent did not create a binding precedent, it notably found that the district court had erred by focusing its inquiry on the undisclosed understanding between the bonds’ issuer and underwriter (the parties that had negotiated and drafted the indenture). That evidence should have been ascribed only minimal weight, the dissenting judge instructed, and the district court should have instead focused more on representations that had been made to the bonds’ purchasers.

As of this blog post’s publication date, the case remains pending on the district court docket for a decision on whether the issuer must pay the make-whole. The Wall Street Journal reported that a gray market had formed for rights to potential make-whole payments on the redeemed bonds, which were trading at a price between 16 and 20 cents. Meanwhile, on December 12, 2014, the issuer petitioned the Second Circuit for a rehearing, arguing that the majority had mistakenly ignored securities industry custom and practice when adopting the compressed timeline interpretation. As always, this blog will keep readers posted on any significant decisions in the case.

Observations and Takeaways

There are a number of lessons to draw from the Chesapeake bond redemption decisions:

- First, the opinions have much to say about the technical nuances of contractual interpretation. One high-level point is that a great deal of legal wrangling can occur at the “plain meaning versus ambiguity” stage of textual analysis, without any regard for the true intentions of the drafters or parties in interest.

- Second, contractual meaning is frequently in the eye of the beholder. It is notable (though not surprising) that every party and judge involved in the case worked with the same interpretive framework and many of the same canons of construction. Each interpretation – whether or not it carried the day – was supported with meticulous reasoning. Yet different conclusions were reached for different reasons. That is not unique to this case, and is important to remember.

- Third, interpreters not only frequently reach different views on meaning, but their disagreement can be vehement. Take, for example, the district court opinion, which concluded that the condensed-window interpretation “did violence” to another sentence in the indenture, was “at war” with the basic canons of construction, and was commercially unreasonable, tortured, and even incoherent. Interpretation is the bread and butter of a legal professional, so when you step into this arena be ready for idiosyncrasies and strong feelings.

- Fourth, and more generally, a strong view on meaning is frequently necessary, particularly when litigating – but not always. One can be well served by taking counsel from someone who is able to step out from themselves to appreciate where the various interpretive tools and approaches leave room for play. A skilled, dispassionate eye for detecting the contours of interpretive disputes can be invaluable when making document-driven decisions and when looking for value-add litigation opportunities. As Chesapeake shows, a latent ambiguity uncovered at the wrong (or right) time can play out in a zero-sum game.

- Fifth, Chesapeake shows what can happen when drafters do not keep the right audience in mind. Many attorneys take pride in their ability to cleverly resolve deal points with a functional, but convoluted, mechanic, and others are content to draft using words and provisions simply because everyone else at the negotiating table knows what they mean. But when contractual language taken out of context and scrutinized by those from outside a particular industry (as is often the case in bankruptcies), that language has to stand on its own. For that reason, drafting with absolute clarity and precision is essential.

More from the Restructuring Blog

Copyright © 2026 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Prior results do not guarantee a similar outcome. Weil, Gotshal & Manges LLP is headquartered in New York and has office locations in Austin, Boston, Brussels, Dallas, Frankfurt, Hong Kong, Houston, London, Los Angeles, Miami, Munich, New York, Paris, San Francisco, Silicon Valley and Washington, D.C.